Best Debt Relief Programs of 2026: Companies That Can Help You Settle Unsecured Debt

The content of this material is informational and educational in nature and cannot be regarded as financial advice. It is extremely important to conduct an independent analysis before any financial transactions. If you are not sure about financial matters, it is strongly recommended to seek the advice of an independent expert.

When standard monthly payments stop being workable, debt relief programs offer a structured path forward — through settlement negotiations, a debt management plan, or consolidation. Finding the best debt relief companies of April 2026 means looking closely at fees, minimum debt thresholds, timelines, accreditations, and where each provider actually operates. This guide to the best debt relief companies of 2026 covers seven providers in depth, followed by a comparison table, cost breakdown, eligibility guidance, and alternatives.

The best debt relief programs reviewed in this guide

| Product | Features | Rating | Link | |

|---|---|---|---|---|

|

National Debt Relief |

Active across ~45 states, D.C., and U.S. territories — the widest state footprint on this list — with broad eligibility for unsecured balances. | 4.9/5 | Visit Site | |

|

Accredited Debt Relief |

Works as both a direct settlement firm and a matching service, routing clients toward settlement, consolidation, or credit counseling based on their profile. | 4.8/5 | Visit Site | |

|

Freedom Financial Network |

The only provider in this review offering a money-back program guarantee, triggered when total settlement costs exceed the original enrolled balance. | 4.7/5 | Visit Site | |

|

TurboDebt |

Highest Trustpilot rating among all seven providers here; operates as both a direct settlement company and a matching platform across most U.S. states. | 4.6/5 | Visit Site | |

|

ClearOne Advantage |

Active in 48 states — the widest reach on this list — and reports serving over 170,000 clients since launching in 2008. | 4.5/5 | Visit Site | |

|

JG Wentworth |

Over 30 years in financial services, with a built-in legal-partner network for clients who face creditor lawsuits while enrolled. | 4.4/5 | Visit Site | |

|

Americor |

The only debt settlement company in this group that also functions as a direct lender, offering in-house consolidation loans through affiliated lender Credit9. | 4.3/5 | Visit Site |

Top Debt Relief Companies of 2026 Compared

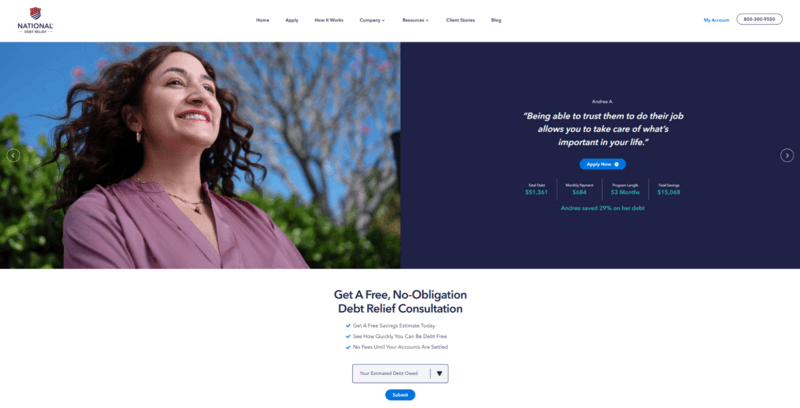

National Debt Relief – Lowest Minimum Debt, Widest State Reach

National Debt Relief reports having resolved $11.5 billion in enrolled debt since 2009 for 1.3 million clients. Its $10,000 minimum debt requirement matches most providers on this list; fees of 15%–25% apply post-settlement only — no upfront charges.

State coverage is broad, though the program excludes OR, VT, and WV. Fees reach 25% in some states, and credit score damage is expected during enrollment.

| Category | Details |

| Best for | Wide state availability, established track record |

| Type of help | Debt settlement |

| Min. debt | $10,000 |

| Fees | 15%–25% enrolled debt + account fees |

| Program length | 24–48 months |

| Main debt types | Credit cards, medical, personal loans, student loans, business debt |

| Availability | ~45 states + D.C., PR, GU, USVI |

| Accreditation | A+ BBB, IAPDA Platinum, ACDR, AADR |

Pros:

- $10,000 minimum debt; accepts credit cards, medical bills, personal loans, student loans, and business debt — a wider range than most providers here

- Available in ~45 states + D.C., PR, GU, USVI

- No upfront fees; charged post-settlement only

- Named Forbes Advisor’s best debt relief company for 2026 — four years running

Cons:

- Fees reach 25% in some states, reducing net savings

- Not available in OR, VT, or WV; mortgages, auto loans, federal student loans excluded

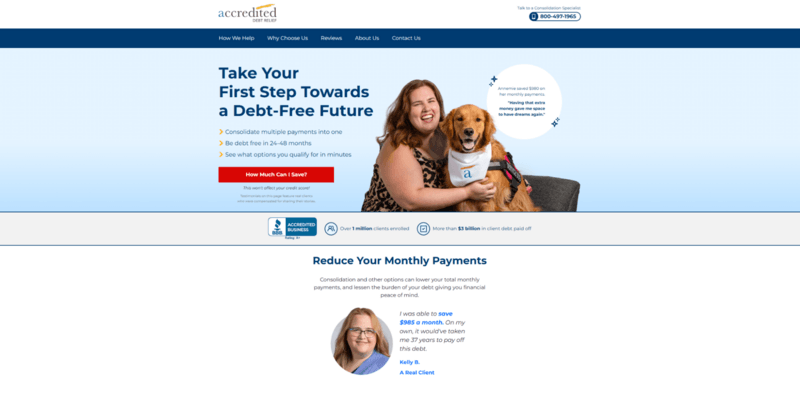

Accredited Debt Relief – Multi-Path Debt Relief Matching for 2026

Accredited Debt Relief runs as both a settlement firm and a matching platform, steering clients toward settlement, consolidation, or credit counseling. Accredited Debt Relief provides free consultations; fees of 18%–25% of enrolled debt apply post-settlement only.

While Accredited Debt Relief offers debt settlement in ~30 states only — narrower than most — fees frequently hit the 25% ceiling, and credit score damage is standard during enrollment.

| Category | Details |

| Best for | Multi-option matching, free consultations |

| Type of help | Debt settlement + partner matching |

| Min. debt | $10,000 |

| Fees | 18%–25% enrolled debt + account fees |

| Program length | 12–48 months |

| Main debt types | Credit cards, medical, personal loans, private student loans |

| Availability | ~30 states + D.C. |

| Accreditation | A+ BBB, AADR, IAPDA-certified arbitrators |

Pros:

- A single intake process covers settlement, debt consolidation, and credit counseling options

- Free consultation and soft credit pull with no commitment required

- A+ BBB rating; AADR member; IAPDA-certified arbitrators

- Named Bankrate’s Best for Customer Satisfaction in 2026

Cons:

- Limited to ~30 states, excluding many consumers across the U.S.

- Fees often reach 25%; account serviced by parent Beyond Finance may cause confusion

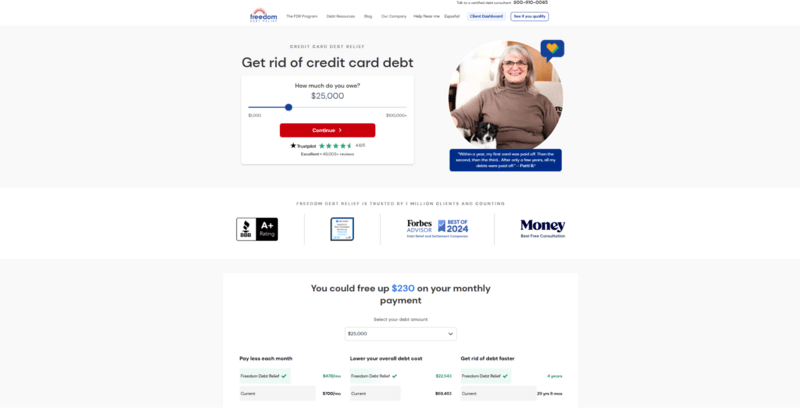

Freedom Financial Network – Industry’s Only Money-Back Program Guarantee

Freedom Financial Network is unique for its money-back program guarantee — if total costs exceed enrolled debt, up to 100% of fees are refunded. Since 2002, the company reports settling $20 billion for 1 million clients.

State coverage reaches ~39 states, with several excluded. Fees run 15%–25% of enrolled debt, and credit score damage is expected throughout enrollment.

| Category | Details |

| Best for | Money-back guarantee |

| Type of help | Debt settlement |

| Min. debt | $10,000 |

| Fees | 15%–25% enrolled debt + account fees |

| Program length | 24–48 months |

| Main debt types | Credit cards, personal loans, medical, business cards, private student loans |

| Availability | ~39 states |

| Accreditation | A+ BBB, IAPDA Platinum, ACDR founding member |

Pros:

- Only company here with a money-back program guarantee

- $10,000 minimum debt; accepts credit cards, personal loans, medical bills, business cards, and private student loans

- A+ BBB; IAPDA Platinum; founding member of ACDR

- Seven-day support, client app, and legal-partner network included

Cons:

- Excludes CO, KS, OR, SC, VT, WV, WI; mortgages, auto loans, federal student loans not accepted

- Credit score damage expected; fees reach 25% in some states

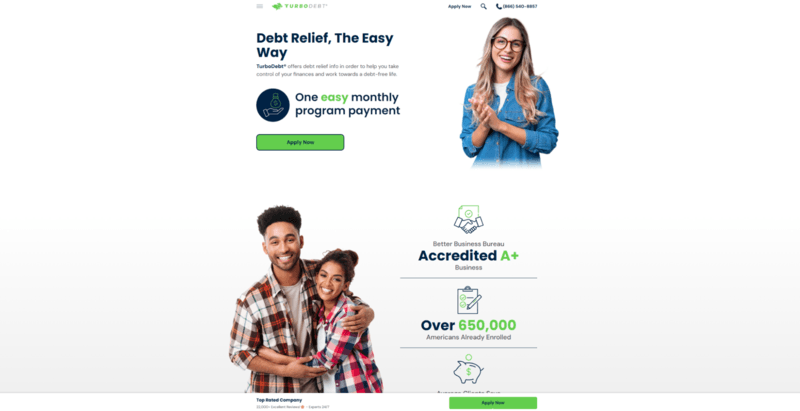

TurboDebt – Highest Trustpilot Rating Among 2026 Debt Relief Programs

Founded in 2020, TurboDebt runs as both a direct provider and a matching platform — routing clients to debt settlement, credit counseling, or debt management. Its 4.9/5 Trustpilot rating tops this review.

TurboDebt often acts as a matcher rather than a direct servicer — always confirm who manages your account before enrolling. Fees reach 25%.

| Category | Details |

| Best for | High ratings, hybrid matching service |

| Type of help | Debt settlement + partner matching |

| Min. debt | $10,000 |

| Fees | 15%–25% enrolled debt; partner-set |

| Program length | 24–48 months |

| Main debt types | Credit cards, personal loans, medical, business debt, payday loans |

| Availability | Most U.S. states |

| Accreditation | A+ BBB, AADR, ACDR, IAPDA-certified arbitrators |

Pros:

- 4.9/5 Trustpilot — highest rated debt relief service in this review

- Covers most U.S. states; broad eligibility including payday loans

- A+ BBB, AADR, ACDR, IAPDA-certified — strong accreditation

- No upfront fees; settlement fee applied post-settlement only

Cons:

- Often acts as a matching service — a third party may manage your account and set fees

- $10,000 minimum debt excludes those with smaller balances

ClearOne Advantage – Widest State Reach on This 2026 List

Active in 48 states — the widest coverage of any company in this review — ClearOne Advantage reports serving 170,000+ clients since 2008, with over $3 billion in debt resolved.

Fees reach up to 29% of enrolled debt — the highest ceiling in this review. Some customers report credit score impact, slow communication, or difficulty cancelling.

| Category | Details |

| Best for | Broad state coverage, established track record |

| Type of help | Debt settlement |

| Min. debt | $10,000 |

| Fees | 18%–29% enrolled debt + ~$17/mo |

| Program length | 24–48 months |

| Main debt types | Credit cards, personal loans, medical bills, private student loans |

| Availability | 48 states (excludes IL, OR) |

| Accreditation | A+ BBB, ACDR, IAPDA-certified, DFPI-registered |

Pros:

- Active in 48 states — the widest state availability in this entire review

- 170,000+ clients served; over $3 billion in debt resolved since 2008

- A+ BBB, ACDR, IAPDA-certified specialists

- Extended weekend and weekday support via phone, chat, email

Cons:

- Highest fee ceiling in this review — up to 29% plus a monthly account fee

- The BBB has noted a complaint pattern; some clients report cancellation difficulties

JG Wentworth – 30-Year Brand with Built-In Legal Partner Access

JG Wentworth has over 30 years in financial services and has served 150,000+ clients. Fees of 18%–25% of enrolled debt apply post-settlement; no cancellation charge.

Coverage spans 30 states — fewer than most. Some clients report undisclosed monthly fees and restrictions on paying off the program early. Credit score damage is expected.

| Category | Details |

| Best for | Established brand, legal access |

| Type of help | Debt settlement, debt resolution |

| Min. debt | $10,000 |

| Fees | 18%–25% enrolled debt + account fees |

| Program length | 24–60 months (avg. 42 months) |

| Main debt types | Credit cards, medical, personal loans, private student loans |

| Availability | 30 states + D.C. |

| Accreditation | A+ BBB, AADR, IAPDA-certified arbitrators |

Pros:

- More than 30 years in financial services; 150,000+ clients served

- Legal-partner network included for clients dealing with creditor lawsuits

- A+ BBB; AADR member; IAPDA-certified arbitrators; no cancellation fees

- Broader marketplace with insurance and personal loan options

Cons:

- Available in only 30 states, limiting access for many U.S. consumers

- Some clients report undisclosed monthly fees and restrictions on paying off the program early

Americor – Only Debt Settlement Company That Also Lends Directly

The only debt settlement company in this review operating as a direct lender, Americor debt relief offers debt consolidation loans to $48,000 through affiliated lender Credit9.

Unlike most debt relief services, Americor debt relief charges no setup or monthly fees. Fees of 14%–29% of enrolled debt apply post-settlement, and credit score damage is expected during enrollment.

| Category | Details |

| Best for | Direct lender, no monthly fees |

| Type of help | Debt settlement + consolidation loans |

| Min. debt | $10,000 |

| Fees | 14%–29% enrolled debt; no setup/monthly fees |

| Program length | 20–48 months |

| Main debt types | Credit cards, personal loans, medical, student loans |

| Availability | Most states (excl. CO) |

| Accreditation | A+ BBB, AADR, IAPDA |

Pros:

- Only debt settlement company here offering in-house debt consolidation loans

- No setup or monthly account fees — unlike most debt relief companies

- A+ BBB; AADR; IAPDA-certified; most U.S. states

- 4.7/5 Trustpilot across 16,000+ reviews; 450,000+ clients served

Cons:

- Fees reach up to 29% — the highest top end among companies in this review

- Some clients report being pitched high-APR consolidation loans alongside settlement programs

How We Chose the Best Debt Relief Programs

Finding the best debt relief companies takes more than comparing advertised savings. The companies on this list were assessed by practical value, fee transparency, customer protection, and accreditation. Cost differences and risk disclosure often matter more than headlines.

- Fee transparency and total cost. Settlement fees in the debt relief industry typically run 15%–25% of enrolled debt, with some reaching 29%. Monthly account fees were also reviewed.

- Minimum debt requirement. The minimum debt requirement is $10,000 across all providers on this list, consistent with the standard for the debt settlement programs reviewed.

- Program timeline. Most programs run 24–48 months. Realistic completion rates and early-exit terms were considered alongside advertised timelines.

- Types of debt accepted. Coverage of credit cards, medical bills, personal loans, and private student loans was reviewed. Companies that accept a wider range of debt types scored higher.

- Reputation, reviews, and accreditation. BBB ratings, Trustpilot scores, and complaint history were reviewed alongside certification through the International Association of Professional Debt Arbitrators and the Association for Consumer Debt Relief.

- State availability. Accessibility across U.S. states was considered. Programs limited to 30 states or fewer were noted as a significant restriction.

- Customer support and progress tracking. Whether a debt management dashboard, app, or dedicated account manager is included matters for the borrower’s ability to monitor the program.

- Risk and transparency disclosures. How clearly each company discloses credit score impact, tax implications on forgiven debt, and legal limitations was weighted heavily — not treated as secondary information.

No debt relief provider should be judged solely on potential savings. Total fees, realistic risks, honest process disclosure, and whether the required monthly deposits are manageable for the borrower all deserve equal weight.

What Is a Debt Relief Program?

Debt relief is an umbrella term for any structured approach to resolving outstanding consumer debt. Relief is an umbrella covering several distinct services — each designed for different financial situations, debt types, and hardship levels. The term gets used loosely across programs that work in very different ways. Understanding each type of debt relief before enrolling matters.

Approaches commonly grouped under debt relief include:

- Debt settlement — a company negotiates with creditors to accept less than the full balance owed

- Debt negotiation — similar in concept, sometimes handled directly with the creditor or through an attorney

- Debt management plan — a structured debt management program through a nonprofit agency, usually with reduced interest rates and waived fees

- Credit counseling — professional review of income, debt, and available options through organizations like the National Foundation for Credit Counseling; often the recommended starting point before choosing any program

- Debt consolidation — combining multiple debts into a single loan, typically depending on the borrower’s creditworthiness

- Bankruptcy guidance or attorney referrals — a legal route for the most severe cases, requiring qualified counsel

Some of these approaches — debt settlement being the most common — reduce the total amount owed. Others focus on lowering interest, simplifying payments, or helping the borrower understand which debt relief program is best suited to their specific situation.

One important limitation: the companies on this list focus on unsecured consumer debt — primarily credit card debt, personal loans, and medical bills. Mortgages, auto loans, federal student loans, child support, and most tax debts fall outside what a standard debt relief program covers. Assuming these will be included is a common mistake that leads to problems after enrolling.

How Debt Relief Programs Usually Work

How debt relief works isn’t always straightforward — the steps below reflect a typical settlement-based program. The general debt relief process can shift significantly based on the company, type of debt, and the borrower’s overall situation.

- Request a consultation — The customer calls or submits a form and walks through their debts and financial situation.

- Review — Total debt amount, debt types, income, hardship level, and what the borrower can realistically contribute monthly are all weighed up here.

- Program recommendation — The review shapes which debt relief approach is right. Settlement doesn’t suit every caller or every debt situation.

- Dedicated account setup — In settlement programs, the customer redirects monthly deposits into a dedicated savings account rather than paying enrolled creditors. Those creditor payments stop. Once funds have built up enough, negotiations can start. Missing deposits risks stalling the program.

- Negotiation — When saved funds are sufficient, the company contacts creditors and works toward settlements on the enrolled debt.

- Settlement approval — Each offer is sent back to the customer for review and sign-off before any funds are released.

- Program completion or exit — The debt settlement process runs until enrolled debts are resolved, or until the customer chooses to leave.

Outcomes vary. Creditor cooperation, state rules, company practices, and the customer’s ability to sustain monthly deposits all play a role. Credit scores typically drop during enrollment — accounts go delinquent as savings accumulate, which is part of how the process works.

Worth flagging: creditors have no legal requirement to accept settlement offers. Entering into a debt settlement program doesn’t guarantee every account gets resolved, and some creditors may take legal action during the process. Debt settlement is also quite distinct from a debt consolidation loan, which replaces debts with a new loan rather than negotiating a reduction on the total enrolled debt.

Main Types of Debt Relief

Choosing the right type of debt relief comes down to the debt amount, the type of debt involved, the borrower’s credit situation, and how much they can realistically manage each month.

Debt Settlement

Debt settlement works by negotiating unsecured debt down to less than the full balance owed. It ranks among the most widely used debt settlement services, particularly for large credit card or personal loan balances. Results are never guaranteed, and the credit score will typically take a hit.

Debt Negotiation

The mechanics overlap closely with settlement — creditors are approached directly about adjusting repayment terms or reducing the outstanding balance. Some borrowers manage it independently; others use a licensed attorney or a third-party debt settlement firm.

Debt Management Plan

A debt management plan keeps repayment going but typically lowers interest rates and wraps everything into one monthly payment. Run through a nonprofit as a structured debt management program, it doesn’t cut the principal — but it helps borrowers get out of debt without the credit damage that settlement causes.

Credit Counseling

Budget, type of debt, and available options — that’s what credit counseling helps borrowers review. It’s usually free or low-cost, and consumer debt relief through nonprofit counseling is often the recommended first step before choosing any program.

Debt Consolidation Loan

A debt consolidation loan bundles multiple debts — credit cards and personal loans being the most common — into a single new monthly payment. Creditworthiness and the available interest rate determine whether it makes sense.

Balance Transfer Card

A balance transfer card works for some borrowers with good credit who have the discipline to pay off the balance before the promotional period ends. Transfer fees and post-promotion rates apply.

Bankruptcy Guidance

Bankruptcy is a legal process for the most severe debt situations and requires working with a qualified attorney. The relief can be significant, but the long-term impact on credit score and financial history is very real.

Who Debt Relief May Be Suitable For — and Who Should Avoid It

Debt relief may not suit every borrower. Knowing where it works — and where it doesn’t — can prevent a costly mistake.

Who May Consider Debt Relief

Debt relief tends to make sense for borrowers who are already behind or close to it. Specific situations include:

- Significant unsecured debt — credit cards, medical bills, personal loans — with no realistic way to reduce the balance

- Missed or consistently late payments with no improvement in sight

- Unable to qualify for debt consolidation due to a damaged credit score

- Monthly minimum payments are no longer manageable on the current income

- Considering bankruptcy but looking for an alternative that avoids formal proceedings

The amount of debt matters. All programs on this list require $10,000 to enroll — and the approach only works when the total consumer debt load genuinely can’t be managed through regular payments.

Who Should Avoid It or Compare Alternatives First

Some borrowers are not well-matched to debt settlement or similar programs:

- Most of the debt is secured — mortgages, auto loans, or home equity lines don’t qualify

- Federal student loans are involved — these are not eligible and have dedicated federal relief options

- The borrower can still get out of debt through regular payments within a reasonable timeframe

- There isn’t enough monthly cash flow to fund the required dedicated account deposits

- Expectations are unrealistic — no company can guarantee specific outcomes or timelines

Approaching any debt relief program with realistic expectations and a clear understanding of the risks matters.

What Debts Usually Qualify for Debt Relief

Debt relief doesn’t apply to every balance a borrower holds. Most programs center on unsecured consumer debt — balances where no collateral backs what’s owed. Which accounts qualify and which don’t can depend on the provider, creditor, state rules, debt status, and profile.

Commonly eligible:

- Credit card debt — the largest and most common type of debt enrolled in settlement programs

- Unsecured personal loans with no asset attached

- Medical bills, hospital collections, and other medical-related balances

- Collection accounts and charged-off balances from original creditors or collectors

- Some private student loans, depending on the lender and the provider

- Some business debts, if the company specifically supports them

Usually harder to include or not suitable:

- Mortgages and home equity debt — secured, with the property as collateral

- Auto loans — secured against the vehicle

- Any other secured loan where an asset backs the balance

- Federal student loans — handled through government programs with dedicated options; outside the scope of private settlement

- Child support, alimony, and court-directed financial obligations

- Most tax debts, unless they go through a tax relief specialist

- Utility bills and very small balances that most companies won’t enroll

The total debt amount and the status of each account — whether still current, delinquent, or in collections — also affect eligibility. Many providers won’t negotiate on accounts that haven’t missed any payments. Knowing which type of debt qualifies before reaching out saves time and avoids surprises.

Fees, Costs, and Timelines

Understanding the full cost of a debt relief program before signing matters as much as the advertised savings. Debt relief companies typically present projected results upfront, but actual costs depend on variables not always visible in the headline.

How fees work

Companies typically charge between 15% and 25% of enrolled debt for debt settlement — some reach 29%. The key question is whether the fee applies to enrolled debt (the balance at sign-up) or settled debt (the negotiated final figure). Most use enrolled debt, so the amount of your debt at enrollment — not the outcome — drives the fee. What any debt relief offers in projected savings should be weighed against this calculation.

Most providers also charge a one-time setup fee ($9–$10) and a monthly maintenance fee ($9.85–$17) for the dedicated savings account.

Other costs to factor in

During a debt settlement program, enrolled accounts go unpaid while negotiations continue. Interest, late fees, and penalty rates accrue throughout — the total amount of debt reaching settlement is often higher than the opening balance. Any forgiven amount of $600 or more typically triggers an IRS Form 1099-C, which may affect tax liability and carry implications for your credit score.

Upfront fees violate the FTC’s Telemarketing Sales Rule — debt relief companies typically charge only after each settlement is finalized. The minimum debt threshold, monthly deposit size, and creditor response all influence program length. Timelines run 24–48 months.

| Cost item | What to check |

| Settlement fee | Percentage and whether charged on enrolled or settled debt |

| Dedicated account fee | Setup and monthly maintenance amount |

| Accruing interest | Balances continue growing until each debt resolves |

| Tax consequences | Forgiven debt may trigger IRS Form 1099-C |

| Upfront fee | Any charge before settlement is complete is a legal violation |

| Total enrolled debt | Opening balance used for all fee calculations |

Risks and Downsides

Weighing the pros and cons of debt relief before enrolling is as important as comparing fees. The cons of debt relief don’t always surface in promotional materials — but they’re significant.

Credit and financial risks

Credit score damage is expected and often severe during debt settlement enrollment. Accounts go delinquent, charge off, and get reported as settled — all negative marks that stay on a credit report for up to seven years. Most borrowers see credit score drops of 100+ points during the program.

Interest, late fees, and penalty rates continue accumulating on unpaid balances. By the time settlement negotiations begin, the total balance may be meaningfully higher than when enrollment started.

Creditors aren’t required to negotiate. Some refuse entirely — particularly with for-profit debt settlement firms. Others respond by filing lawsuits, which can result in wage garnishment or bank levies. Most settlement programs don’t include legal defense as standard, leaving borrowers to handle this separately.

Tax and fee risks

Forgiven debt of $600 or more typically generates a Form 1099-C from the lender, treating the canceled amount as taxable income. Insolvency at the time of forgiveness may reduce or eliminate the tax liability, but it requires filing IRS Form 982 — not automatic.

Program fees of 15%–29% can erode the apparent savings significantly, especially when combined with accruing balances during the process. Consumer debt relief rarely produces the net savings figures promoted in upfront marketing.

Scam risk

The debt relief industry carries meaningful fraud risk. Companies guaranteeing specific outcomes, demanding upfront payment, or claiming government affiliation are red flags under FTC guidelines. Debt resolution outcomes can’t be promised — any company suggesting otherwise should be avoided.

Working with a credit counselor or nonprofit agency before signing up for any settlement program can help identify whether alternatives are a better fit first.

How to Apply for a Debt Relief Program

Deciding to enroll in a debt relief program is only one part of the process. Preparation before the first consultation makes the rest significantly easier.

Step 1: Log each debt

Pull together every account — creditor name, current balance, interest rate, minimum payment, and how overdue each one is. This builds an honest picture of your total debt from the start and lets the provider assess which accounts qualify.

Step 2: Identify which accounts to include

Not every account needs to go in. Secured debts won’t qualify, and some smaller balances may be easier to handle independently. Decide in advance which debt to enroll and which to pay off separately.

Step 3: Know your finances

Providers will ask about income and expenses. Know your credit score going in — it sets realistic expectations about consolidation alternatives and helps avoid being steered toward the wrong product.

Step 4: Estimate a realistic monthly deposit

Each month, you deposit a fixed amount into a dedicated account. Always pick a figure that’s genuinely affordable. Overestimating it is a common reason programs stall.

Step 5: Run quotes from two or three providers

Look at what each company offers — fee structure, minimum debt requirements, state availability, and timeline estimates. Don’t accept a quote from one provider only.

Step 6: Ask the right questions

Before signing anything, ask about fee calculation method, cancellation rights, who administers the dedicated account, and what happens if a creditor refuses to negotiate.

Step 7: Read the full agreement

Every debt settlement contract must include FTC-required disclosures. Read them. Anything unclear or absent should be addressed in writing before you sign anything.

How to Choose the Best Debt Relief Company

Choosing the right debt relief company means matching specific criteria to your situation — not just picking the first name that comes up.

Check accreditation before anything else

The American Association for Debt Resolution (AADR) and the Association for Consumer Debt Relief (ACDR) are the two main industry bodies. IAPDA certification confirms that the arbitrators handling your case are qualified. Any debt relief company should hold at least one of these credentials, and it should be independently verifiable.

Compare fee structures carefully

Most debt relief companies offer fees of 15%–25% of enrolled debt — some reach 29%. Always confirm whether the percentage applies to the original balance or the settled amount, then add setup and monthly costs to reach the actual total.

Check the minimum debt requirement

The minimum debt requirement is $10,000 across all providers on this list. If your balance falls below that threshold, confirm eligibility before spending time on a full consultation.

Verify state availability

Some providers operate in only 30 states; ClearOne Advantage covers 48. Don’t book a consultation until you’ve confirmed the company is properly licensed to operate in your state.

Review the program type

Not every provider handles the same approach. Some offer debt management options or referrals to credit counseling alongside settlement. If you want to consolidate your debt rather than settle, confirm the company actually covers that path.

Look at reputation data

BBB rating, Trustpilot score, CFPB complaint history, and total review volume all matter. Your credit score takes a hit during any settlement program — a provider’s completion track record matters as much as its advertised fee.

Ask about support and legal access

Find out how debt relief providers handle creditor lawsuits. Most don’t include legal defense. A few — including Freedom Debt Relief and JG Wentworth — offer attorney network access. If you’re already facing collection action, that distinction matters.

The table below covers what to look for when trying to find the best debt relief program for your situation.

| What to check | Why it matters |

| Accreditation (AADR, ACDR, IAPDA) | Verifies conduct standards and confirms arbitrators hold certification |

| Fee basis (enrolled vs. settled debt) | Which amount applies shifts your total cost — often by a lot |

| Minimum debt requirement | Filters out non-qualifying providers right away |

| State availability | Unlicensed providers can’t legally help you regardless |

| Program type | Knowing the model stops you picking the wrong type |

| Reputation data | Pattern of real outcomes, not just promotional claims |

| Legal access | Rarely included; know before trouble starts |

Alternatives to Debt Relief Programs

A debt relief program isn’t the only route. Credit profile, overall debt load, and monthly cash flow shape which of several alternatives to debt relief may deliver a better result at lower long-term cost.

DIY repayment methods

The debt avalanche — pay the highest-rate balance first — and the debt snowball — clear the smallest balance first — are both solid, proven ways to get out of debt alone. Neither harms your credit, and the only cost is the payments you’re already making.

Direct creditor negotiation

Calling creditors directly to request hardship programs, temporary rate reductions, or lump-sum settlement offers often produces the same outcome as working through a third party — without the 15%–25% fee. Many major issuers have documented hardship programs that never get advertised.

Free credit counseling

NFCC-member agencies and the Association for Consumer Debt Relief both run free or low-cost credit counseling. Sessions typically cover budgeting, a debt review, and referrals to structured options. Consumer debt relief through a nonprofit route is typically less damaging to credit and carries lower fees than settlement.

Debt management plan

A debt management plan through a nonprofit agency reduces interest rates and consolidates payments without touching the principal. Monthly fees are usually under $50. A debt management program typically runs 36–60 months and preserves credit better than debt settlement.

Debt consolidation loan

Banks, credit unions, and online lenders all offer a debt consolidation loan that wraps several balances into a single payment. A FICO score of roughly 640 is the usual floor to consolidate your debt. A personal loan used for consolidation typically carries APRs of 6%–36%.

Balance transfer

Moving high-interest credit cards to a 0% intro-rate card reduces interest for 12–21 months. This only works if the balance is payable before the promotional period ends.

Bankruptcy

Chapter 7 or Chapter 13 may resolve debt faster and more cleanly than years of settlement — especially when the debt load is severe. A qualified attorney consultation is the right first step.

Frequently Asked Questions

Can I keep one credit card open while using a debt relief program?

Yes, if the card isn’t among the enrolled accounts. Most programs only require you to stop paying the specific credit cards or debts included in the plan. That said, some issuers monitor credit reports and may close other accounts once delinquencies appear elsewhere. A secured card from an unrelated credit union is the safest option.

What documents should I prepare before a consultation?

Recent statements for all accounts, proof of income, a basic monthly budget, your most recent credit report, any collection notices or lawsuit paperwork, and a rough list of your assets. No legitimate provider needs your bank account number on the first call.

Can a debt relief company work with joint or co-signed debts?

Yes, but enrolling a shared unsecured debt affects both parties’ credit. The co-signer should be informed — ideally agree — before payments stop. Some providers require signatures from both borrowers before adding a joint account.

What happens if my income changes during the program?

Most providers can adjust the monthly deposit amount. A significant income drop may extend the timeline or push you toward debt management or another approach. Notify your provider as soon as anything changes.

Can I leave a debt relief program early?

Yes. Federal rules allow cancellation at any time, and the funds in your dedicated account belong to you. Any enrolled debt that hasn’t been settled yet incurs no fee — but the credit score damage from missed payments has already happened by then.

Will creditors keep calling after I enroll?

Yes, often more frequently. Most companies send a limited power of attorney to creditors requesting calls be directed elsewhere, but creditors aren’t required to comply. Collection activity typically continues throughout the program.

Can I use debt relief if I’m not behind on payments yet?

Technically yes, but most creditors won’t negotiate until accounts are 90–180+ days delinquent. Enrolling while current means stopping payments immediately, which triggers credit damage right away. A debt settlement program works better as a last resort — not a first response.