Best RuPay Credit Card in India: 10 Cards That Actually Reward Your UPI Payments

The content of this material is informational and educational in nature and cannot be regarded as financial advice. It is extremely important to conduct an independent analysis before any financial transactions. If you are not sure about financial matters, it is strongly recommended to seek the advice of an independent expert.

RuPay credit cards work differently in India. They link directly to UPI apps, so you earn rewards on small daily payments—something Visa and Mastercard can’t do. This guide breaks down the best rupay credit card options for 2026. You’ll see how rewards work, what UPI cashback rates look like, which cards charge annual fees, and who gets lounge access. We’ve covered cards from HDFC Bank, Axis Bank, ICICI Bank, and others. Looking for high UPI rewards? Want a lifetime-free option? Prefer Tata ecosystem perks? This article explains what matters when choosing a rupay credit card that fits how you actually spend money in India’s credit card market.

Check out these 10 top RuPay credit cards in India for 2026:

| Product | Features | Rating | Link | |

|---|---|---|---|---|

Tata Neu RuPay Credit Card |

Shop at BigBasket or Croma? You can earn 10% through NeuCoins that spend like actual rupees | 4.9/5 | START | |

ICICI RuPay Credit Card |

ICICI's starter option delivers UPI rewards and works everywhere in India | 4.9/5 | START | |

ICICI Coral RuPay Credit Card |

Movie buffs save 25% at BookMyShow twice monthly, plus lounge access every quarter | 4.8/5 | START | |

HDFC Pixel RuPay Credit Card |

Pick your own 5% cashback categories, plus you'll get 1% back on UPI via PayZapp | 4.7/5 | START | |

IDFC RuPay Credit Card |

Existing IDFC users add this digital card for 3X rewards when UPI spends cross ₹2,000 | 4.7/5 | START | |

HDFC Bank UPI RuPay Credit Card |

Just ₹99 yearly gets you 3% on groceries—India's cheapest UPI card | 4.5/5 | START | |

HDFC MoneyBack+ RuPay Credit Card |

Amazon and Flipkart shoppers rack up 10X rewards for ₹500 annual fee | 4.6/5 | START | |

Axis Bank SuperMoney RuPay Credit Card |

Zero fees forever, 3% UPI cashback through super.money app | 4.4/5 | START | |

IndusInd Bank Platinum RuPay Credit Card |

Free card, 2% on UPI, no monthly caps—just your credit limit | 4.3/5 | START | |

YES BANK Paisabazaar PaisaSave RuPay Credit Card |

Virtual card pays 6% on restaurants and flights, 1% on UPI over ₹2,000 | 4.5/5 | START |

Top 10 RuPay Credit Cards India 2025

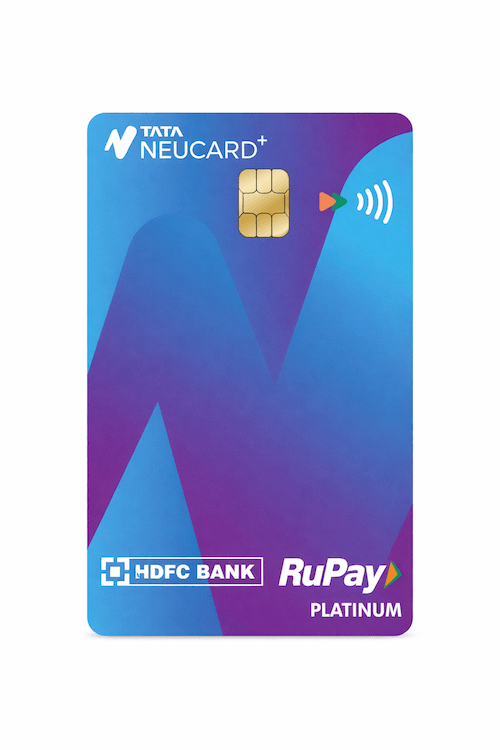

Tata Neu RuPay Credit Card – Best for Tata Ecosystem Shoppers

Tata Neu Infinity makes sense if you’re already buying from BigBasket, Croma, or Westside. You’ll earn 5% NeuCoins on Tata brands, plus another 5% bonus if you’re a NeuPass member—that’s 10% total. Regular spends outside Tata get 1.5% back. NeuCoins convert rupee-for-rupee when you redeem them.

The ₹1,499 annual fee sounds steep until you realize HDFC gives you 1,499 NeuCoins as a welcome bonus. That basically covers your first year. Waive future fees by spending ₹3,00,000 annually. UPI payments through the Tata Neu app earn 1.5%, but other UPI apps like GPay only give 0.5%. There’s a 500 NeuCoin monthly cap on UPI rewards.

Lounge access changed in June 2025. Now you need to spend ₹50,000 each quarter to unlock 2 domestic lounge visits. International travelers get 4 visits yearly through Priority Pass. Groceries, utilities, and telecom purchases each cap at 2,000 NeuCoins monthly.

| Key Point | Details |

|---|---|

| Annual fee / waiver | ₹1,499 + GST / Spend ₹3,00,000 yearly |

| Rewards format | NeuCoins (1 NeuCoin = ₹1) |

| UPI benefit | 1.5% via Tata Neu app, 500 NeuCoins monthly cap |

| Best for | Regular Tata brand shoppers and BigBasket users |

Pros:

- 10% total returns on BigBasket, Croma, Westside, Tanishq purchases

- Welcome bonus offsets first year fee completely

- Milestone-based lounge access (domestic and international)

- Lower 2% forex markup vs typical 3.5%

- Works across entire Tata ecosystem

Cons:

- High ₹3 lakh annual spend needed for fee waiver

- UPI rewards drop to 0.5% outside Tata Neu app

ICICI RuPay Credit Card – Best Entry-Level Option with Wide Acceptance

ICICI’s basic RuPay card serves first-time credit card users who want something straightforward. The bank designed this for people just starting their credit journey in India. You’ll find decent acceptance at most merchants since ICICI has one of the largest banking networks nationwide.

The card comes with a ₹500 plus GST annual fee, though existing ICICI savings account holders often get lifetime-free offers through the iMobile app. Check your pre-approved section regularly if you bank with ICICI. UPI transactions earn reward points at standard rates—nothing spectacular, but they add up over time with regular use.

What makes this card practical is its simplicity. There aren’t complicated reward tiers or spending categories to track. You swipe, you earn points, and redemption works through ICICI’s standard rewards catalog. The bank includes basic insurance coverage and 24/7 customer support.

| Key Point | Details |

|---|---|

| Annual fee / waiver | ₹500 + GST / Often LTF for account holders |

| Rewards format | Standard ICICI Reward Points |

| UPI benefit | Base earning rate on UPI transactions |

| Best for | First-time card users wanting reliable acceptance |

Pros:

- Wide merchant acceptance across India

- Simple reward structure without complex tiers

- Often available as lifetime-free for existing customers

- Backed by ICICI's large banking network

- Good starting card for building credit history

Cons:

- Basic rewards compared to specialized cards

- Limited premium perks or benefits

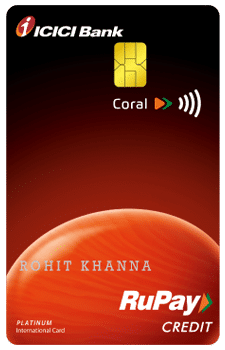

ICICI Coral RuPay Credit Card – Best for Movie Lovers and Entertainment

ICICI Coral delivers real value for people who hit theaters regularly. You’ll save 25% at BookMyShow and INOX—up to ₹100 off, twice every month. The ₹500 plus GST annual fee (₹590 total) disappears when you spend ₹1,50,000 yearly, excluding rent and education payments.

UPI transactions earn roughly 0.5% through reward points—2 points per ₹100 on larger merchants, 1 point on smaller ones. Each point converts to ₹0.25. There’s no explicit monthly cap mentioned, which gives you more flexibility than cards with hard limits. The rewards won’t blow you away, but they’re steady.

Lounge access requires work. Spend ₹75,000 in a quarter to unlock one domestic lounge visit the next quarter. Railway lounges give you 4 free visits yearly without spending requirements. Fuel benefits only apply at HPCL stations—1% waiver on ₹400 to ₹4,000 transactions.

Existing ICICI savings account holders often see lifetime-free offers pop up in the iMobile app. Check your pre-approved section before applying the standard way.

| Key Point | Details |

|---|---|

| Annual fee / waiver | ₹590 total / Spend ₹1,50,000 yearly |

| Rewards format | Reward Points (1 RP = ₹0.25) |

| UPI benefit | ~0.5% effective rate, no explicit cap |

| Best for | Frequent moviegoers wanting entertainment discounts |

Pros:

- 25% BookMyShow/INOX discount twice monthly

- Often available lifetime-free for ICICI account holders

- Railway lounge access without spending requirements

- Milestone-based domestic lounge visits

- ₹2 lakh personal accident insurance

Cons:

- ₹75,000 quarterly spend needed for airport lounge

- Fuel waiver only at HPCL pumps

HDFC Pixel RuPay Credit Card – Best for Customizable Cashback

HDFC’s Pixel Play card stands out because you control where you earn the most. Through the PayZapp app, you pick two spending categories that’ll give you 5% cashback. E-commerce gets 3% automatically, and UPI payments earn a flat 1%. This setup works well if your spending habits don’t fit the usual molds.

The card isn’t free—you’ll pay ₹500 plus GST upfront and annually. But spend ₹20,000 in your first 90 days and HDFC waives the joining fee. Hit ₹1,00,000 yearly and the annual fee disappears too. Your UPI cashback caps at 500 CashPoints monthly, which equals ₹500 since each point converts one-to-one.

What you won’t get here is lounge access. The card focuses purely on cashback returns. Fuel purchases do get a 1% surcharge waiver up to ₹250 per billing cycle. Swiggy Dineout users save an extra 10% when booking through the platform.

| Key Point | Details |

|---|---|

| Annual fee / waiver | ₹500 + GST / Spend ₹1,00,000 yearly |

| Rewards format | CashPoints (1 point = ₹1) |

| UPI benefit | 1% flat rate, 500 points monthly cap |

| Best for | Digital spenders who want control over reward categories |

Pros:

- Choose your own 5% cashback categories

- 3% automatic cashback on all e-commerce purchases

- 1% UPI rewards with straightforward conversion

- Swiggy Dineout offers 10% extra savings

- Fuel surcharge waiver available

Cons:

- ₹500 annual fee unless you spend ₹1 lakh yearly

- No airport lounge access included

IDFC RuPay Credit Card – Best Digital Add-On for UPI Rewards

IDFC’s digital RuPay card works only as an add-on—you can’t get it standalone. Existing IDFC FIRST cardholders add this virtual card to their account for ₹199 plus GST annually. It’s purely digital, so there’s no physical card involved. The whole point is unlocking UPI rewards on your existing credit limit.

The 3X rewards kick in when your UPI transactions cross ₹2,000. Anything below that earns just 1X. This structure benefits people making larger UPI payments rather than small daily purchases. IDFC gives you 100% cashback up to ₹200 as a welcome offer—that’s ₹50 back on each of your first four UPI transactions within 15 days.

If you already hold IDFC’s WOW! Black or Gaj cards, they waive the ₹199 fee completely. Otherwise, you’re paying for the privilege of earning UPI rewards. Fuel purchases don’t earn any rewards, which limits the card’s overall utility compared to others.

| Key Point | Details |

|---|---|

| Annual fee / waiver | ₹199 + GST / Free for WOW! Black, Gaj holders |

| Rewards format | Reward Points (1 RP = ₹0.25) |

| UPI benefit | 3X rewards on UPI above ₹2,000 per transaction |

| Best for | IDFC cardholders making large UPI payments |

Pros:

- Triple rewards on UPI spends over ₹2,000

- Welcome cashback offer worth ₹200

- No separate credit limit needed

- Fee waived for premium cardholders

- Instant digital issuance

Cons:

- Requires existing IDFC FIRST credit card

- Small UPI transactions under ₹2,000 earn minimal rewards

HDFC Bank UPI RuPay Credit Card – Best Budget-Friendly UPI Rewards Card

HDFC’s UPI-focused card costs just ₹99 plus GST annually—India’s cheapest option for earning rewards on UPI payments. Like IDFC’s offering, this works as a floater card against your existing HDFC credit card. You can’t apply for it standalone. The bank issues it as a virtual card that shares your main card’s credit limit.

Groceries and dining earn 3% CashPoints through UPI. Utilities get 2%, while everything else earns 1%. Each category caps at 500 points monthly, which converts to ₹125 since one CashPoint equals 25 paise. Your maximum monthly benefit across all categories hits ₹375. Spend ₹25,000 yearly and HDFC waives the annual fee.

HDFC throws in a ₹250 gift voucher when you make your first transaction within 37 days of activation. That basically covers two years of fees upfront. The card doesn’t offer lounge access or fuel benefits—it’s purely about maximizing UPI rewards at minimal cost.

| Key Point | Details |

|---|---|

| Annual fee / waiver | ₹99 + GST / Spend ₹25,000 yearly |

| Rewards format | CashPoints (1 point = ₹0.25) |

| UPI benefit | 3% groceries/dining, 2% utilities, 500 points per category cap |

| Best for | Existing HDFC cardholders wanting cheap UPI rewards |

Pros:

- Lowest annual fee at just ₹99

- Triple rewards on grocery and dining UPI spends

- ₹250 welcome voucher covers two years of fees

- Easy ₹25,000 annual spend for fee waiver

- Works alongside your existing HDFC card

Cons:

- Add-on only, needs existing HDFC card

- Low point value at ₹0.25 per CashPoint

HDFC MoneyBack+ RuPay Credit Card – Best for E-Commerce Shopping

MoneyBack+ targets online shoppers who live on Flipkart and Amazon. You’ll rack up 10X rewards on these platforms, plus Swiggy, BigBasket, and Reliance Smart. The ₹500 annual fee gets waived when you spend ₹50,000 yearly. Every ₹50,000 you spend quarterly earns a ₹500 voucher as bonus reward.

UPI rewards here are weak—just 2 CashPoints per ₹150 spent, which works out to roughly 0.33% effective rate. That’s the lowest among all cards in this comparison. The 500 points monthly cap means you’ll max out UPI benefits at around ₹125 per month. This card isn’t about UPI performance.

Where it shines is e-commerce purchases. Those 10X rewards add up fast if you’re ordering groceries online or shopping during sale events. Fuel gets a 1% surcharge waiver too. The card makes sense for people whose spending tilts heavily toward online platforms rather than physical stores.

| Key Point | Details |

|---|---|

| Annual fee / waiver | ₹500 + GST / Spend ₹50,000 yearly |

| Rewards format | CashPoints (1 point = ₹0.25) |

| UPI benefit | 0.33% effective rate, 500 points monthly cap |

| Best for | Heavy online shoppers on Amazon, Flipkart, Swiggy |

Pros:

- 10X rewards on major e-commerce platforms

- ₹500 voucher every ₹50,000 quarterly spend

- Easy ₹50,000 annual threshold for fee waiver

- 1% fuel surcharge waiver included

- Strong for online grocery and food delivery

Cons:

- Weakest UPI rewards at 0.33% effective rate

- Better alternatives exist for UPI-focused users

Axis Bank SuperMoney RuPay Credit Card – Best for Maximum UPI Cashback

SuperMoney beats every other card here with 3% cashback on UPI—but only through the super.money app. Use GPay or PhonePe instead and you’ll drop to 1%. The combined monthly cap sits at ₹500, which you’ll hit after spending roughly ₹16,667 via super.money. That caps your annual UPI cashback at ₹6,000 maximum.

There’s zero joining fee and zero annual fee—ever. This lifetime-free status makes it risk-free to hold even if you don’t use it heavily. Cashback lands directly in your account rather than converting through points, which simplifies everything. You’ll also get 1% back on non-UPI spends, capped within that same ₹500 monthly limit.

Fuel purchases earn a 1% surcharge waiver up to ₹400 per cycle on transactions between ₹400 and ₹4,000. The card excludes wallet loads, rent, insurance, and government payments from cashback entirely. Axis issues this as invite-only through the super.money app or to existing Flipkart Credit Card holders.

| Key Point | Details |

|---|---|

| Annual fee / waiver | ₹0 (Lifetime Free) |

| Rewards format | Direct cashback (not points) |

| UPI benefit | 3% via super.money app, ₹500 monthly cap |

| Best for | UPI-heavy users willing to use super.money app exclusively |

Pros:

- Highest 3% UPI cashback rate available

- Zero fees forever—completely free

- Direct cashback without point conversion hassles

- Physical card issued at no cost

- Exclusive merchant offers on Ola, Myntra, MakeMyTrip

Cons:

- Must use super.money app for 3% rate

- ₹500 monthly cap limits heavy spenders

IndusInd Bank Platinum RuPay Credit Card – Best Lifetime-Free Card with Solid UPI Rewards

IndusInd’s Platinum card gives you 2 reward points per ₹100 on UPI spends—roughly 1.2% effective rate when you redeem for non-cash rewards. Regular spends earn just 1 point per ₹100. The lifetime-free structure means you’ll never pay joining or annual fees, which makes it easy to hold long-term.

The monthly cap ties to your credit limit per statement cycle rather than a fixed rupee amount. This flexibility helps heavy UPI users who’d quickly max out cards with ₹500 monthly limits. Fuel gets a 1% waiver capped at ₹100 monthly on transactions between ₹400 and ₹4,000.

Redemption splits into two categories. Cash redemptions give you ₹0.40 per point but cap at 2,500 points monthly. Non-cash options—statement credit, airmiles, vouchers—offer better value at ₹0.60 per point without monthly restrictions. The card includes ₹25 lakh personal accident insurance and ₹2.25 lakh travel coverage.

One unique perk: rent payments via UPI carry zero additional charges. Most cards either block rent or add processing fees.

| Key Point | Details |

|---|---|

| Annual fee / waiver | ₹0 (Lifetime Free) |

| Rewards format | Reward Points (1 RP = ₹0.40-0.60) |

| UPI benefit | 2 RP per ₹100 (~1.2%), cap based on credit limit |

| Best for | UPI users wanting no caps and zero fees |

Pros:

- Lifetime free with no hidden fee requirements

- Double rewards on all UPI transactions

- Monthly caps tied to credit limit, not fixed amount

- Zero charges on rent payments via UPI

- Solid insurance coverage included

Cons:

- Lower cash redemption value at ₹0.40 per point

- No airport lounge access on base variant

YES BANK Paisabazaar PaisaSave RuPay Credit Card – Best for Dining and Travel Cashback

PaisaSave hands you 6% cashback on restaurants and travel—the highest rate in these categories. That caps at ₹3,000 monthly. Everything else earns 1% without limits. The catch with UPI? You only get that 1% on transactions above ₹2,000. Smaller UPI payments earn absolutely nothing.

This comes as a virtual RuPay card alongside a physical Mastercard. The RuPay portion stays lifetime-free while the Mastercard charges ₹499 plus GST from year two. Spend ₹1,20,000 annually and YES Bank waives the Mastercard renewal fee. New YES Bank customers qualify—existing cardholders can’t apply.

Welcome perks include 3-month Zomato Gold Mini, 6-month PharmEasy Plus, a ₹750 Cleartrip voucher, and 500 POPcoins. The forex markup hits 3.40%, which is average. Fuel purchases don’t earn rewards at all—they’re completely excluded from the cashback structure.

The 6% dining cashback makes sense if you eat out frequently or order through Swiggy and Zomato regularly. Travel bookings through platforms like MakeMyTrip also hit that 6% rate.

| Key Point | Details |

|---|---|

| Annual fee / waiver | ₹0 RuPay (LTF), ₹499 Mastercard from Year 2 |

| Rewards format | Reward Points (1 RP = ₹1 statement credit) |

| UPI benefit | 1% cashback only on transactions above ₹2,000 |

| Best for | Frequent diners and travelers seeking category cashback |

Pros:

- Highest 6% cashback on dining and travel

- RuPay variant stays lifetime-free

- Strong welcome benefits package worth ₹1,000+

- Virtual card issued instantly

- Unlimited 1% on all other non-category spends

Cons:

- UPI rewards only apply above ₹2,000 per transaction

- Existing YES Bank cardholders can't apply

Compare All 10 RuPay Credit Cards at a Glance

Picking from 10 different cards? Looking at them side-by-side helps. We’ve pulled the crucial stuff into one table—what you’ll pay, how rewards work, UPI perks, and each card’s strongest point. Scan this first, then dig into the cards that catch your eye.

| Credit Card | Annual Fee | Rewards Type | UPI Benefit | Key Perk | Best For |

|---|---|---|---|---|---|

| Axis Bank SuperMoney | ₹0 (LTF) | Direct cashback | 3% via super.money app | ₹500 monthly cap | UPI maximizers |

| Tata Neu Infinity | ₹1,499 | NeuCoins | 1.5% via Tata app | 10% on Tata brands | Tata ecosystem shoppers |

| IndusInd Platinum | ₹0 (LTF) | Reward Points | 2 RP per ₹100 (~1.2%) | Credit limit-based cap | Heavy UPI users |

| HDFC Pixel | ₹500 | CashPoints | 1% flat rate | Customizable 5% categories | Digital spenders |

| YES PaisaSave | ₹0 RuPay | Reward Points | 1% (>₹2,000 only) | 6% dining/travel | Restaurant lovers |

| HDFC UPI RuPay | ₹99 | CashPoints | 3%/2%/1% tiered | Cheapest UPI card | Budget-conscious |

| IDFC Digital | ₹199 | Reward Points | 3X (>₹2,000) | Digital add-on | IDFC cardholders |

| ICICI RuPay | ₹500 | Reward Points | Base rate | Wide acceptance | First-time users |

| ICICI Coral | ₹590 | Reward Points | ~0.5% | 25% BookMyShow discount | Movie enthusiasts |

| HDFC MoneyBack+ | ₹500 | CashPoints | 0.33% | 10X on e-commerce | Online shoppers |

Two cards won’t cost you anything—Axis SuperMoney and IndusInd Platinum both stay free forever. Shopping mainly at Tata brands? Neu Infinity pays you back the most. Want control over your cashback categories? Pixel lets you choose.

What is RuPay Credit Card and How It Works

RuPay’s India’s own card network, created and run by the National Payments Corporation of India. It works like Visa or Mastercard, except it was built specifically for Indians. When you swipe a rupay credit card, your payment doesn’t bounce through international servers—it stays right here in India through NPCI’s system.

Here’s what happens when you pay: You tap at a store. That payment ping goes to RuPay’s network first. RuPay passes it to your actual bank—HDFC, Axis, whoever gave you the card. Your bank checks if you’ve got credit available and says yes or no. Takes maybe three seconds total.

The network itself isn’t lending you anything. Your bank sets your limit, your interest rate, all that. RuPay just shuffles payment info between shops and banks. Keeping everything domestic cuts processing costs compared to cards that route overseas.

What separates rupay credit cards from others? UPI linking. Connect your RuPay card to GooglePay or PhonePe and suddenly you’re paying with credit by scanning QR codes. Visa and Mastercard can’t do this in India yet. That’s why RuPay caught on for small everyday stuff—chai, autos, vegetables—where whipping out a physical card seems like overkill.

RuPay Credit Card vs Visa/Mastercard (In One Minute)

Three main differences matter. One, UPI works perfectly with RuPay but not other networks. Two, Indian merchants widely accept RuPay—you won’t have problems. Three, using it abroad depends on which card you got. Some RuPay cards work internationally through partner networks, others don’t leave India.

Processing fees usually run cheaper on RuPay since money doesn’t cross borders. Banks often price their RuPay cards lower than Visa or Mastercard versions because of this.

RuPay Credit Cards on UPI (What You Can Do)

Linking a rupay credit card to UPI apps transforms how you handle small payments. You can pay neighborhood stores, street vendors, and local shops by scanning their QR codes—all using your credit line instead of draining your bank account. Bill payments, mobile recharges, and online shopping through UPI-enabled sites all work the same way.

The rewards structure varies wildly by card. Some give you flat cashback rates on all UPI spends. Others tier rewards based on merchant categories—groceries might earn 3% while utilities get 2%. A few cards use points systems where you collect rewards to redeem later. Tata Neu pays in NeuCoins that work only within their ecosystem.

Watch out for caps and exclusions. Most cards limit UPI rewards to ₹500 or similar amounts monthly. Hit that ceiling and you’ll earn nothing extra regardless of spending. Certain categories get blocked entirely—rent, government payments, wallet loads, and insurance premiums typically earn zero rewards even via UPI.

Here’s what makes UPI credit cards useful:

- Daily micro-transactions become rewarding – That ₹50 chai or ₹200 vegetable purchase now earns points

- QR codes beat card swipes for speed – Faster checkout at busy stores and markets

- Credit float on small purchases – Pay later for everyday items without touching savings

- Reward caps favor distributed spending – Spreading purchases across categories maximizes returns

- Not always the best choice – Direct bank UPI or debit cards sometimes offer better deals on utilities

- Transaction minimums matter – Some cards like YES PaisaSave only reward UPI above ₹2,000

- App-specific rates vary – Axis SuperMoney gives 3% through super.money but drops to 1% on GooglePay

Check your card’s fine print before assuming all UPI spends earn rewards. The merchant category, transaction amount, and which UPI app you’re using all affect what you’ll actually get back.

Types of RuPay Credit Cards

RuPay cards split into different tiers based on who you are and how much you earn. Knowing these levels helps you figure out which ones you’ll actually get approved for and what changes when you level up.

RuPay Classic

These target people getting their first credit card or earning modest salaries. Rewards stay basic—you’ll see 0.5% to 1% on regular purchases. Fees rarely cross ₹500 yearly, and many come free. Your credit limit probably won’t exceed ₹50,000 to ₹1 lakh unless you’re pulling in serious income.

Classic cards don’t bother with fancy stuff like airport lounges. They’re about establishing credit history while you earn simple cashback or points on daily spending. If you’ve never owned a credit card, start here.

RuPay Platinum

Mid-range cards that boost rewards and raise limits. You’ll get 1% to 2% back on most stuff, with higher rates for specific categories. Annual fees run ₹500 to ₹1,000. Limits typically stretch from ₹1 lakh up to ₹3 lakhs.

Platinum rupay cards throw in limited lounge visits—maybe 2 to 4 free entries yearly. Fuel waivers become standard. Insurance improves over Classic versions. Banks want you earning ₹25,000 to ₹40,000 monthly if you’re salaried.

RuPay Select

Premium tier where benefits really jump. Reward rates hit 2% to 5% in your best categories. Annual fees climb toward ₹1,500 to ₹3,000. Credit limits start around ₹3 lakhs and can cross ₹10 lakhs for big earners.

Select cards bundle multiple lounge passes, concierge help, and solid travel insurance. You’ll get golf privileges and priority support. Need monthly income above ₹50,000 or strong ITR documents.

RuPay Ekaa

Super-premium level for seriously wealthy folks. Costs upwards of ₹5,000 yearly but delivers luxury—unlimited global lounge access, personal relationship managers, exclusive deals. Most people won’t qualify unless they’re spending ₹20 lakhs plus annually.

Key Features and Benefits of RuPay Credit Cards

Good rupay credit cards in india deliver practical advantages beyond just borrowing money. Here’s what you should expect from a solid card and why these features actually matter in daily use.

- Rewards and cashback programs – Most cards return 0.5% to 3% on purchases through points or direct cashback. Premium cards push this to 5% or even 10% in specific categories like groceries or travel. The format matters—NeuCoins only work in Tata stores while direct cashback lands in your account without restrictions. Check redemption rules before getting excited about high reward rates.

- UPI integration advantage – This is where rupay credit cards beat Visa and Mastercard completely. Link your card to any UPI app and suddenly street vendors, small shops, and local businesses become credit-worthy purchases. You’ll earn rewards on transactions as small as ₹50, which other networks can’t match in India’s UPI-dominated payment landscape.

- Fuel surcharge waivers – Cards typically waive the 1% fuel surcharge on transactions between ₹400 and ₹4,000. Caps usually sit around ₹250 to ₹400 monthly. Not huge savings, but it adds up if you’re filling tank twice weekly.

- Airport lounge access – Premium cards offer 2 to 8 complimentary domestic lounge visits yearly. International access through Priority Pass comes with select variants. Most cards now tie this to spending milestones—you’ll need to hit quarterly thresholds to unlock visits.

- Security features built-in – OTP verification on online purchases, instant SMS alerts, and the ability to set transaction limits through mobile apps. You can block the card instantly if something feels wrong. RuPay’s domestic processing means faster fraud detection compared to international networks.

- Redemption flexibility – Better cards let you convert points to statement credit, essentially getting cash back. Others restrict you to vouchers or specific brand catalogs, which limits actual value. Check how easily you can use accumulated rewards before applying.

- International usage capability – Some RuPay variants work abroad through Discover and JCB partnerships. Forex markups range from 2% to 3.5%. Verify international acceptance before traveling—not all RuPay cards leave India despite what marketing claims.

RuPay Acceptance in India and Abroad

RuPay cards work at millions of shops across India—physical stores and websites both. You won’t have problems at grocery chains, restaurants, petrol pumps, or online shopping sites. Basically anywhere that takes cards will take yours. ATMs? They all work, though pulling cash from credit cards costs you serious fees—avoid that.

International use gets messier. “RuPay International” cards team up with Discover, JCB, and Diners Club for overseas acceptance. But this doesn’t mean they work everywhere globally—you’re stuck with wherever those partner networks reach. Popular spots in Southeast Asia, the Middle East, and some European cities accept these partnerships. Still patchy compared to Visa or Mastercard’s reach.

Planning to travel abroad with your rupay credit card? Check these first:

- Confirm your card works internationally – Look for “RuPay International” printed on it or just call your bank

- Switch on foreign transactions – Most cards block overseas use automatically; flip this setting in your app or through customer service

- Know what forex costs – You’ll pay 2% to 3.5% extra on foreign currency plus possible DCC fees if shops offer to charge you in rupees

- Pack a backup card – Don’t bet everything on RuPay abroad; bring Visa or Mastercard just in case

- Save support numbers – Store your bank’s international helpline before you fly out

- Test it early – Buy something small online in dollars or euros while you’re still home to make sure it actually works

Inside India, rupay cards are widely accepted across merchant outlets in india without issues. Overseas needs homework and backup plans to dodge payment disasters.

How to Link RuPay Credit Card to UPI Apps

Connecting your rupay credit card to UPI platforms takes about five minutes. The process stays pretty similar whether you’re using GooglePay, PhonePe, Paytm, or BHIM, though exact menu names shift slightly between apps.

Start by opening your preferred UPI app. Look for sections labeled “Payment Methods,” “Credit Card,” or “Link Card”—different apps hide this in different spots. Tap the option to add a credit card and select your bank from the issuer list.

You’ll need your card details ready—16-digit card number, expiry date, and CVV from the back. Type these in carefully. The app sends an OTP to your registered mobile number for verification. Enter that code within the time limit.

Next comes setting your UPI PIN specifically for credit card transactions. This PIN differs from your regular card PIN or UPI PIN for bank accounts. Pick a 4 or 6-digit code you’ll remember but others can’t guess easily. Some banks require you to authenticate this through their own banking app as an extra security layer.

| Step | What to Do |

|---|---|

| 1 | Open your UPI app and find “Credit Card on UPI” or similar section |

| 2 | Select “Add Credit Card” and choose your bank name |

| 3 | Enter card number, expiry date, and CVV carefully |

| 4 | Complete OTP verification sent to registered mobile |

| 5 | Set a unique UPI PIN for credit transactions |

| 6 | Make a small test payment (₹10-50) to confirm it works |

| 7 | Check reward posting rules and monthly caps in card terms |

| 8 | Save your card issuer’s support contact for troubleshooting |

Once linked, scan any UPI QR code and pick your credit card as the payment source. Your UPI app will ask for that PIN you just set. Done—you’re paying with credit through UPI.

Fees and Hidden Charges to Watch Out For

Annual fees are just the beginning. Banks hide multiple charges in fine print that can drain your rewards if you’re not watching carefully. Here’s what actually costs you money beyond the obvious stuff.

Joining and annual fees with waiver conditions – Most cards charge ₹500 to ₹1,500 yearly. Waiver thresholds vary wildly—some need ₹50,000 annual spend, others demand ₹3,00,000. Miss that target and you’re paying the full fee. The joining fee sometimes gets waived separately from annual renewal, so read both conditions.

Interest-free period and late payment penalties – You get 20 to 50 days interest-free if you pay your full statement balance. Miss the due date by even one day? You’ll face 25% to 42% annual interest on your entire outstanding amount plus late fees of ₹500 to ₹1,300 depending on how much you owe.

Cash withdrawal charges hurt badly – Drawing cash from ATMs using credit cards costs 2.5% to 3% upfront plus interest starts immediately with no grace period. A ₹10,000 withdrawal can cost you ₹250 to ₹300 just in fees before interest even kicks in.

Reward redemption fees and restrictions – Some banks charge ₹99 to ₹250 for converting points to cash or vouchers. Minimum redemption thresholds block you from using small point balances.

Fuel surcharge waiver caps – That 1% fuel waiver maxes out at ₹250 to ₹400 monthly. Cross that and you’re paying full surcharges on additional fills.

UPI reward caps and category exclusions – Monthly caps of ₹500 mean your rewards stop regardless of spending. Rent, insurance, government payments, and wallet loads typically earn zero rewards even when paid via UPI.

Forex markup on international transactions – Foreign currency purchases add 2% to 3.5% on top of exchange rates. Some merchants offer DCC (billing in rupees), which adds another 3% to 5% markup—always decline DCC.

GST gets added to everything – Every fee mentioned above gets slapped with 18% GST on top, inflating your actual costs.

Frequently Asked Questions About RuPay Credit Cards

1.

How do I link a RuPay credit card to UPI apps like PhonePe or Google Pay?

Open your UPI app and find “Credit Card” or “Payment Methods” in the menu. Tap “Add Credit Card,” select your bank, then enter your card number, expiry, and CVV. You’ll get an OTP—enter it to verify. Set a UPI PIN specifically for credit transactions. Make a ₹10 test payment to confirm it works. The whole process takes five minutes.

2.

Do RuPay credit cards give rewards or cashback on UPI spends?

Yes, but rates vary wildly. Axis SuperMoney gives 3% via super.money app. Tata Neu pays 1.5% in NeuCoins. HDFC Pixel offers 1% flat. Nearly every card caps UPI rewards monthly at ₹500 or equivalent points. Some cards like YES PaisaSave only reward UPI above ₹2,000. Rent, wallet loads, and insurance don’t earn rewards even via UPI.

3.

Is RuPay accepted everywhere in India, and can I use it abroad?

RuPay works at millions of merchant outlets across India—stores, websites, fuel stations, ATMs. Domestic acceptance matches Visa. International use needs “RuPay International” cards that partner with Discover and JCB networks. Coverage exists in Southeast Asia and Middle East but stays limited versus Visa or Mastercard. Always carry a backup card when traveling abroad. Forex charges run 2% to 3.5%.

4.

RuPay vs Visa: which network is better for everyday use in India?

RuPay wins for India-specific use through UPI integration—Visa can’t link to UPI apps here. You’ll earn rewards on small QR code payments at local shops and street vendors. Processing fees stay lower since transactions remain domestic. Visa offers better international acceptance if you travel frequently. Choose RuPay if spending stays mostly in India with daily UPI use.

5.

Is it possible to get a lifetime-free RuPay credit card, and what are the usual conditions?

Three cards are truly lifetime-free—Axis SuperMoney, IndusInd Platinum, and YES PaisaSave’s RuPay variant. Zero fees forever without spending requirements. Other cards need annual thresholds—HDFC MoneyBack+ requires ₹50,000 yearly while Tata Neu demands ₹3,00,000. Existing bank customers often get lifetime-free offers through mobile apps. Watch for “first year free” tricks that charge from year two.

6.

Can I withdraw cash or transfer money to my bank account from a RuPay credit card?

Yes, but avoid it—extremely expensive. Banks charge 2.5% to 3% immediately as cash advance fees. Interest starts from day one at 25% to 42% annually with no grace period. A ₹10,000 withdrawal costs ₹250-300 upfront plus daily interest. Money transfers get blocked or treated identically. Third-party apps charge extra 1.5% to 3% on top, making it doubly costly.